Why We Invested: Meet the Newest Catalyst Fund Companies

Abalobi from South Africa, created a fisher-driven mobile app suite

Abalobi from South Africa, created a fisher-driven mobile app suite

We’re excited to announce the latest companies to join the Catalyst Fund portfolio! Our new cohort of inclusive fintech startups is innovating in two promising areas: insurance technology (“insurtech”) and digital credit. As a group, these companies exhibit strong founding teams, experience working in emerging markets, and a resolute commitment to reach the underserved. As an early-stage accelerator committed to expanding innovative financial solutions for the the underbanked, we invested in these companies because they share the following qualities:

1. They offer tailored products designed for and with low-income customers

In a global market where only 5 percent of customers access insurance, Brazilian ToGarantido and South African MobiLife are expanding access to high quality, affordable, and tailored insurance products to the financially excluded.

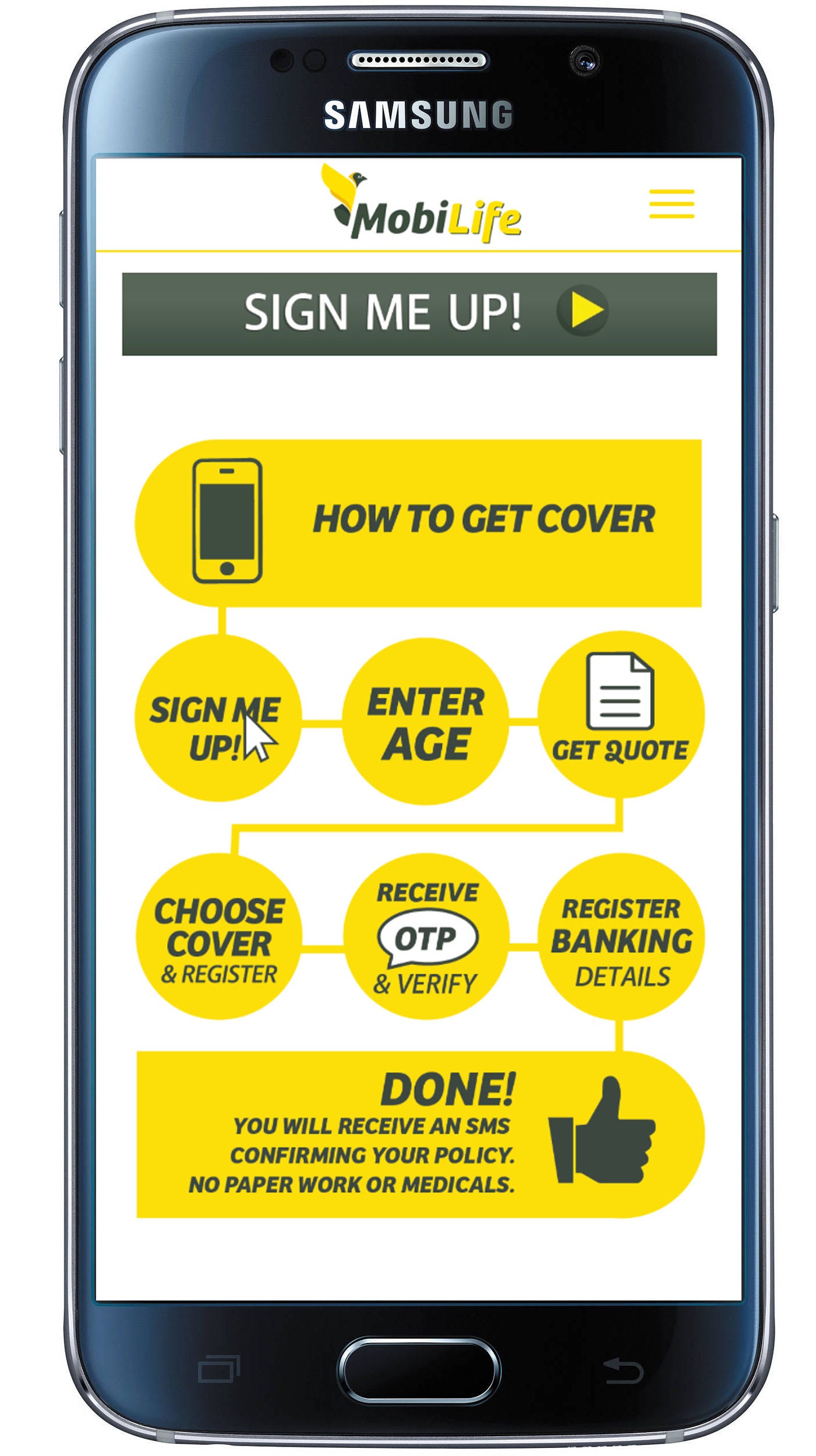

MobiLife recognized that low-income consumers in South Africa required a new type of insurance product. It had to be flexible and could never lapse. Mobilife’s 100 percent mobile insurance products allow customers to skip premiums when needed without risking policy cancellation. They also adapt to the needs of the family unit. FoodSurance, their flagship life insurance product, pays a weekly grocery voucher to a family for up to 5 years after the passing of a breadwinner. This offering matches the food security needs of families after a devastating loss. Mobilife also keeps the customer signup process extremely simple. Customers purchase insurance within minutes on their smartphones. There is no paperwork. No lengthy call center waits. No medical tests required.

Rukula gives low-income consumers small loans to purchase low-value every day goods

Similarly, as the expansion of mobile technology and availability of alternative data is paving the way for more digital credit solutions, the companies Rukula and Asaak are set to improve the quality, and not simply the quantity of credit solutions. Rukula gives low-income consumers small loans to purchase low-value household durables and electronic items through a network of 80 trusted merchants, directly at point of sale. Customers can purchase a new product within 15 minutes of providing support documentation. Rukula has already extended credit to 18,000 Sri Lankans and is growing profitably month on month.

“At Rukula, we give access to items that most people at the top of the pyramid would take for granted and empower Sri Lankan consumers to improve their daily lives,” says Reeza Zarook, CEO of Rukula.

Abalobi leverages a digital value chain to offer payments and other financial services to fishermen in South Africa. Abalobi embraced human-centered design from the get-go and co-created their solutions directly with the low-income fisher folk they serve. Through Abalobi’s “ “hook to cook” system, “fishers are able to access an accounting logbook to log their catches, set fair prices and sell their catch directly to restaurants via a mobile marketplace”, says Serge Raemaekers, CEO of Abalobi. This verified (digital) income stream also gives fishers a formal financial identity, paving the way to co-develop simple and relevant financial services such as loans, savings and insurance for fishers, securing their livelihoods and families.

Watch the Catalyst Fund 2017 video

2. They leverage technology to go down market, improve operations, and make products relatable for customers

As traditional insurers struggle with prohibitive distribution costs and lack of effective communication channels with the low income customer base, To Garantido and Mobilife overcome these barriers with technology. ToGarantido reimagined the way insurance is distributed via a chatbot-automated platform. The chatbot automates the customer acquisition process and gives Brazilian customers, already comfortable online, the experience of interacting with a real person. The friendlier interaction with the chatbots raises customers’ comfort levels to ask questions and allows them to purchase a product without physically visiting a branch or agent, which can be intimidating. Ninety-five percent of ToGarantido customers are receiving insurance for the first time.

Technology also enables a smoother customer verification process to access credit, a major issue for traditional lenders. Asaak, for example, built a mobile tech stack to verify their Ugandan applicants’ collateral within 1 hour via an API integration with the Uganda Ministry of Land, which manages all property records for land, real estate, vehicles, and heavy machinery. Ugandan entrepreneurs and farmers can now access Asaak’s mobile-based collateralized loans in hours, rather than weeks..

3. They craft business models that build trust blending human and digital touches

Because many emerging market consumers are not yet ready for full digitization, ensuring human touch points along the customer journey is critical. Asaak’s “human-enabled digitization model” ensures loan officers meet each new client in person to review their first loan application to establish a personal connection and develop trust.

Similarly, MobiLife uses a network of sales ambassadors to humanize the insurance purchasing experience.

“Just having someone that can explain the benefits of products and facilitate the digital on-boarding is key to create trust with customers,” says Frank Shutte, CEO of MobiLife.

As a portfolio of companies, ToGarantido, MobiLife, Rukula, Asaak and Abalobi have created dynamic business models that blend old and new; integrating digital technology and human touchpoints to better meet the needs of the low-income customer. Although it is still early days, we see their promise and look forward to working together to broaden their reach, spur innovation, and address the myriad challenges they will face as emerging startups.