Three Key Ways that Inclusive Fintech Companies Deepen Financial Inclusion

Customers Value More Affordable, Better Designed and Time-saving Products and Services

1. Tech + Touch: New Interactions to Reach & Keep Customers

Carolina, a building cleaner in Sao Paulo, is worried about providing for her young family with her tight household budget. As sole parent and breadwinner of two children, how can she be prepared for any of life’s mishaps such as an accident or illness? She finds out about ToGarantido, an affordable and fully digital insurance company, serving low- to middle-income consumers in Brazil. On her smartphone, she follows Lara, the ToGarantido chatbot, to apply for a low-premium health insurance plan that can get approved in 7–12 minutes. But she’s unsure about coverage plans and gets redirected to a call center to speak to a real person.

ToGarantido, like other inclusive fintech companies we have worked with, adopted a mix of “tech + touch” to onboard customers and increase their level of trust in services since many customers are not yet ready for a fully digital journey. As a result, ninety percent of ToGarantido’s current customers are accessing insurance for the first time.

2. Tangible & Appropriate Value Propositions

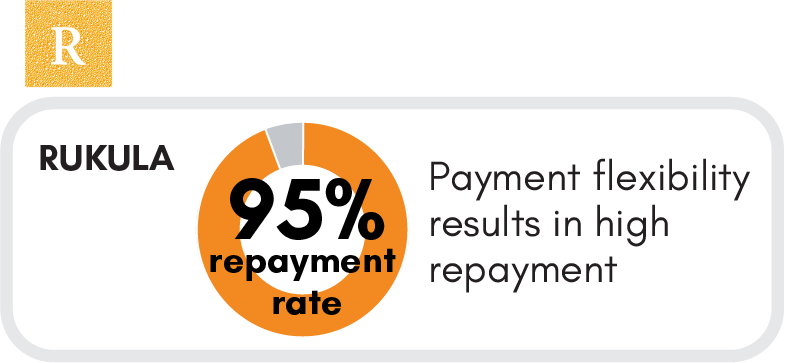

Kavith, a tuk-tuk driver in Colombo, recently purchased on layaway, a new first mobile phone to help him communicate more quickly in his job. His income varies day to day, and this week he will not be able to meet his installment payment. Thanks to payment flexibility from Rukula, a digital lending startup that enables small vendors in Sri Lanka to sell consumer goods on credit without late payment penalties or fees, he is able ultimately to pay off the mobile phone purchase. The extreme flexibility and long-term repayment outlook has paid off for Rukula: 95 percent of loans are paid off within two years.

#CF20 company Rukula is making it possible for people like Kavith to have access to household consumer durables and electronic items to enhance their quality of life.

Likewise, Mobilife, a South African insuretech provider, introduced flexibility in premium payments and holds a three-percent lapse rate compared to an industry average of 50 percent.

Meet Frank Schutte , CEO of Mobilife

#CF20 company Mobilife, Africa’s first 100% “built-for-mobile” life insurance, using the power of smartphones, accessible, fast and flexible insurance solutions to low-income consumers.

3. Reducing Business Cost

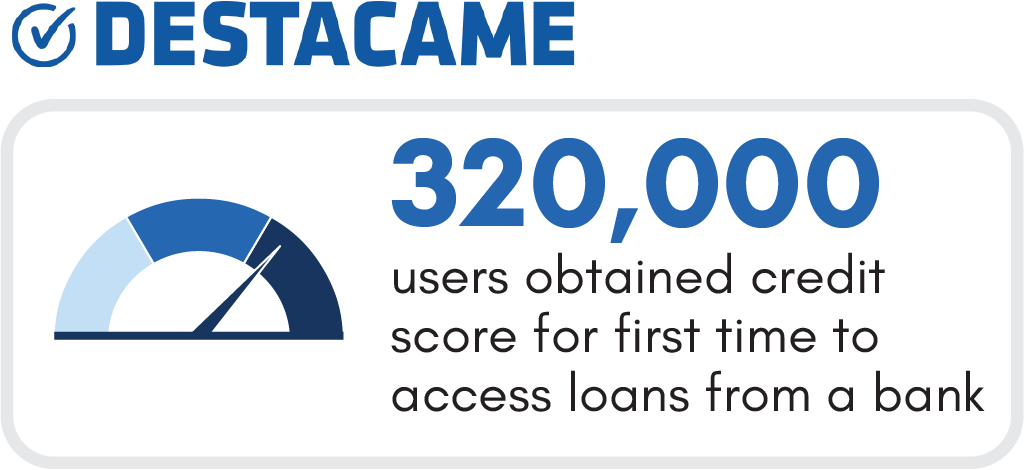

Alejandro, in Santiago, clicked on an ad on Facebook, to obtain his first-ever credit score through Destacame, a Catalyst Fund company in Chile and Mexico that has built a proprietary algorithm to generate alternative credit scores for underbanked customers using their utility payment data. He accessed the low-interest loan for working capital to expand his small pastry business.

Inclusive fintech companies like Destacame leverage the power of modern techniques and tools such as alternative credit scoring and social media to reduce business costs, allowing them to offer lower costs to users. As of 2014, 320,000 Destacame users accessed a credit score for the first time, 200 clients received graduation loans at low interest rates and 80 percent of very low-income customers paid back their loans.

How Far Can Inclusive Fintech Go?

Through BFA’s deep expertise of the low-income markets, financial services and fintech, our initiative, Catalyst Fund, has provided 15 companies to date with tailored technical assistance, accelerating their ability to offer more affordable, better designed and time-saving products and services in industries such as education, energy, employment, retail, agriculture, and fishing to low-income customers. By creating new and superior value propositions, inclusive fintech startups are reaching more low-income populations and increasing their adoption of essential financial services, such as digital payments, loans, and insurance that help low-income people better their livelihoods.

The above scenarios are just some examples of the three approaches that make fintech inclusive — and are available to all providers and actors in the ecosystem. Read our new brief, Proven Strategies for Making Fintech Inclusive by Wajiha Ahmed, Director, Consumer Insights at BFA for a deeper look at driving and broadening financial inclusion.

Don’t miss out on our webinar on November 14 at 9 AM EST as we delve deeper into this topic with the author Wajiha Ahmed. You can register for our webinar here.