Meet KarmaLife, bringing financial services to gig workers in India

Digital platforms in India will employ 15 million people by 2021. While these gig-workers are not formally employed by the platforms, they can earn regularly and their earnings can be tracked via the platform’s digital infrastructure. Together, these two factors make gig-workers’ earnings resemble formal employment, though the amount of their earnings can vary considerably.

However, since they are not recognized as formal, full-time employees, these workers have difficulty accessing mainstream financial services that can help them make ends meet, plan for the future, or improve their business. KarmaLife is partnering with leading digital platforms in India to bring these workers access to credit lines as well as insurance via an app that allows seamless transfers and payments via UPI.

Impact

Although gig workers on digital platforms like Flipkart and Uber can earn regularly and get paid on a predictable basis (i.e., weekly, biweekly, or monthly), they do not have fixed salaries or pay-slips. Their earnings can fluctuate based on variations in the number of orders they deliver and the amount of time they dedicate. For work that includes the use of personal assets (like cars or trucks) the occasional upkeep may add to their costs. Additionally, if competition increases, regulation changes, or adverse global calamities like this pandemic take place, the work can dry up. For example, ride-share and food-delivery companies like Ola and Swiggy have been slashing staff numbers in the past months due to the pandemic even as e-commerce demand has surged.

Given these vulnerabilities, few mainstream financial service providers consider gig workers to be a good financial bet. As a result, most remain on the margins of financial wellbeing with limited access to full-featured credit, insurance or investment products. Instead, they tend to rely on vanilla bank accounts, payment apps, or informal providers. This exclusion is concerning under normal circumstances but is even more urgent given the pandemic as workers, who have proven essential to urban supply-chains, still need services to stabilize income and increase resilience.

As a result, when such workers need access to credit or face emergencies, they ask their employers for loans or turn to money lenders in their communities. This likely takes place frequently as 70% of gig workers noted they were interested in accessing personal loans. Unfortunately, this interest rarely translates into access and 76% of casual workers who needed loans sought them from non-institutional sources. In fact, when one firm started offering financial services to gig workers, they found that 80% of customers were new to formal credit.

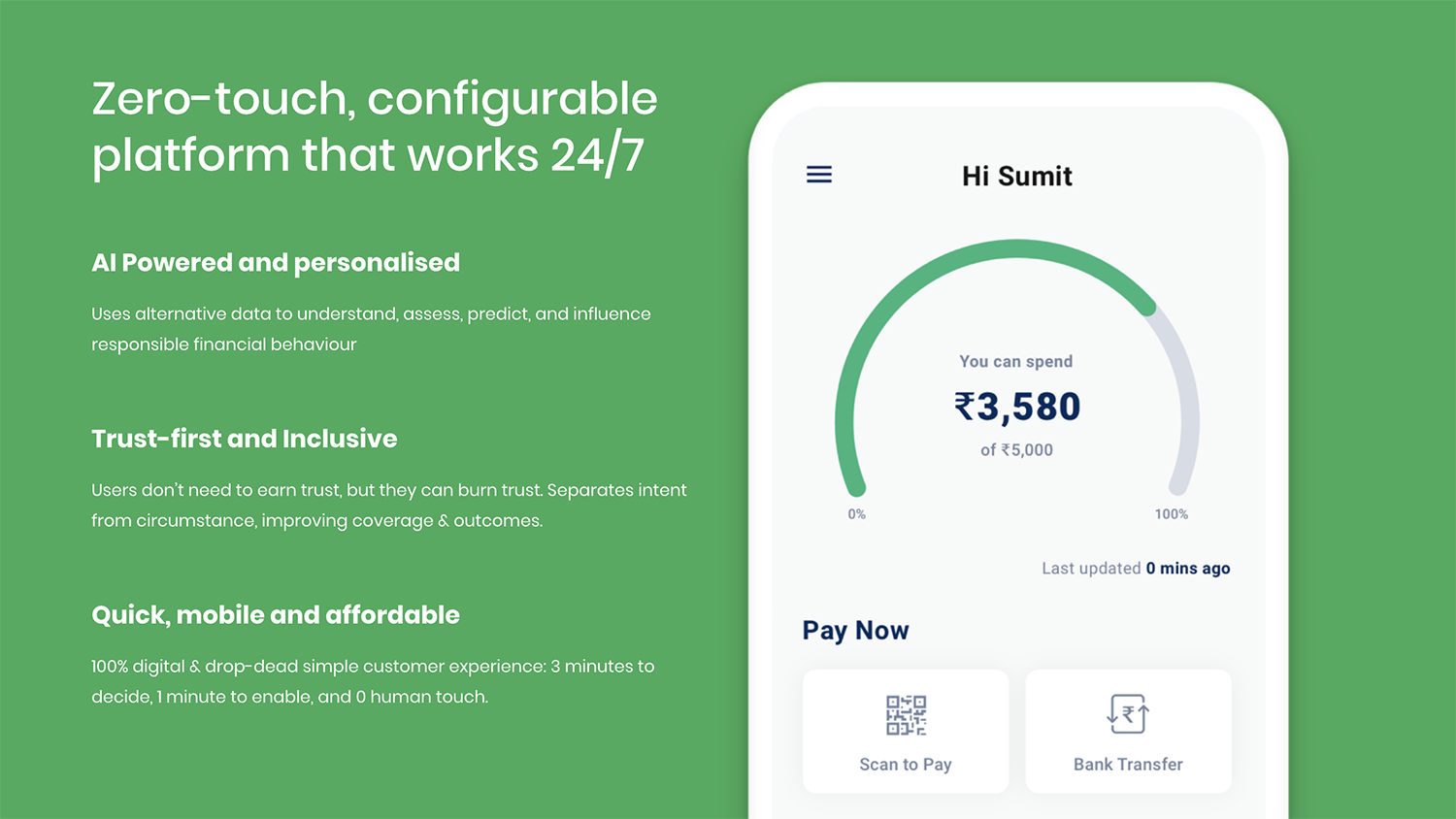

KarmaLife is partnering with the digital platforms that employ these workers to facilitate access to a few benefits, namely access to credit lines and insurance (currently in pilot mode). These platforms pay a subscription fee so that the worker’s KarmaLife account is linked to their payout account from the platform. Platforms report that KarmaLife helps drive greater worker productivity and retention, and is a simple way to offer benefits without the operational costs and headache. KarmaLife provides the platforms with a dashboard so they can track how workers are utilizing the services.

Workers download an app that shows them the extent of their credit line and the amount of credit they have used. The app is directly linked to UPI rails as well as to their bank account so that payments and transfers are seamless.

Not only does KarmaLife make it possible for gig workers to access financial services instantly, without the need for traditional documentation like bank account details or credit scores, but they also do so at rates lower than market alternatives. The credit lines are roughly one-third of the workers’ monthly income, and repayment is flexible as workers can either set up regular deductions or program transfers as convenient.

Innovation

The KarmaLife app delivers on the potential of IndiaStack to dramatically expand access to financial services among marginal and informal workers. The IndiaStack has provided the foundation for 80% of Indians to get a bank account, but other inclusion indicators like ATM density or usage of digital payments are still very low.

By creating a solution that is tailored to the specific income flows of gig-workers and that uses common digital infrastructure, KarmaLife is revolutionizing financial services for workers earning money in new ways. . Their highly-configurable solution can offer customisable loans to gig workers based on their income size, payment cycles, spend controls and other parameters that the partner platforms can offer. They also capture and analyze real-time risk through alternative data to understand gig workers better, adjust the credit limit dynamically to ensure credit access and usage is sustainable.

As such, their product recognizes that gig workers earn regularly and fairly predictably even if with ups and downs, and uses this data to power the financial products. Instead of penalizing the ups and downs of gig work, KarmaLife rewards the consistency of gig work by adapting their loan product to allow flexible repayments and amounts.

We hope that KarmaLife’s approach is the start of a wider set of portable benefits that bring other services like pensions and healthcare to those without formal, full-time jobs, and provide them with a much needed safety net.

Growth potential

Gig and freelance work is growing dramatically, and may soon reach half of the world’s workforce. In the US, nearly 40% of the US workforce takes part in the gig economy, and these numbers may soon be reached in emerging markets like India and Kenya, where platforms are growing dramatically. For example, India’s gig gross volume is projected to grow by 115% by 2023, and the e-commerce market is expected to grow to $200 billion by 2026. Some reports suggest that these numbers may surge further in light of the pandemic.

The growth of e-commerce means there will be many more delivery workers, as well as opportunities for remote workers and MSMEs to sell online. KarmaLife also intends to support other blue-collar workers who form a significant proportion of the local economy such as construction, factory, and domestic workers as they become increasingly digitized.

The Catalyst Fund model has seen outsized success compared with other accelerator programs. We accelerate startups that excel on three fronts:

- Impact: Catalyst Fund startups deliver (or, in the case of B2B firms, facilitate the delivery) of life-changing products and services to underserved populations. These can include financial services like loans, savings, insurance, and investment, but also access to productive inputs or essential services such as energy, sanitation, and water.

- Innovation: Our startups are pioneering game-changers that are innovating new products and business models. They drive the sector forward by demonstration effect and via the learning that Catalyst Fund documents and shares.

- Growth potential: Catalyst Fund startups are distinctively investment worthy, developing businesses that are scalable, with high growth potential. Our startups are selected by an Investor Advisory Committee, who have deep experience in emerging markets and nominate high-potential startups, and then sponsor and mentor them through Catalyst Fund. As a result, our startups raise more funding than startups from other accelerators.