Prosper: A Product Innovation to Link PAYGo Customers to MFIs

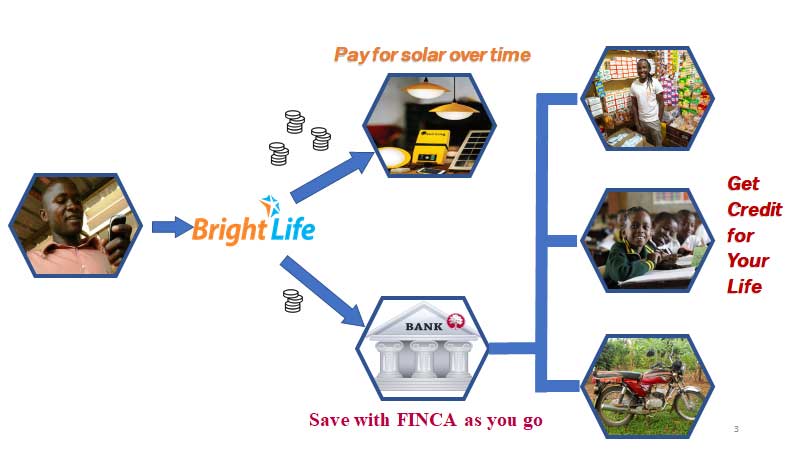

BrightLife, FINCA Uganda, and FIBR are innovating to develop solutions that bridge the gap between microfinance and pay-as-you-go (PAYGo) lending cultures. We designed a product — called Prosper — that graduates unbanked and under-banked PAYGo customers to become clients of an MFI, thereby combining the best qualities of both cultures.

Our previous blog on FIBR’s engagement with BrightLife and FINCA Uganda laid out the case for MFIs to play a larger role in the PAYGo solar sector. In that blog we questioned whether institutions have to choose between MFI and PAYGo approaches to credit (spoiler: no). Here we describe how the two institutions can work together to create a pathway for PAYGo customers to become MFI clients, allowing them to borrow and save securely, create a formal financial identity, and ultimately grow their financial capacity.

Challenges in Design

Challenge #1: Connecting Institutions

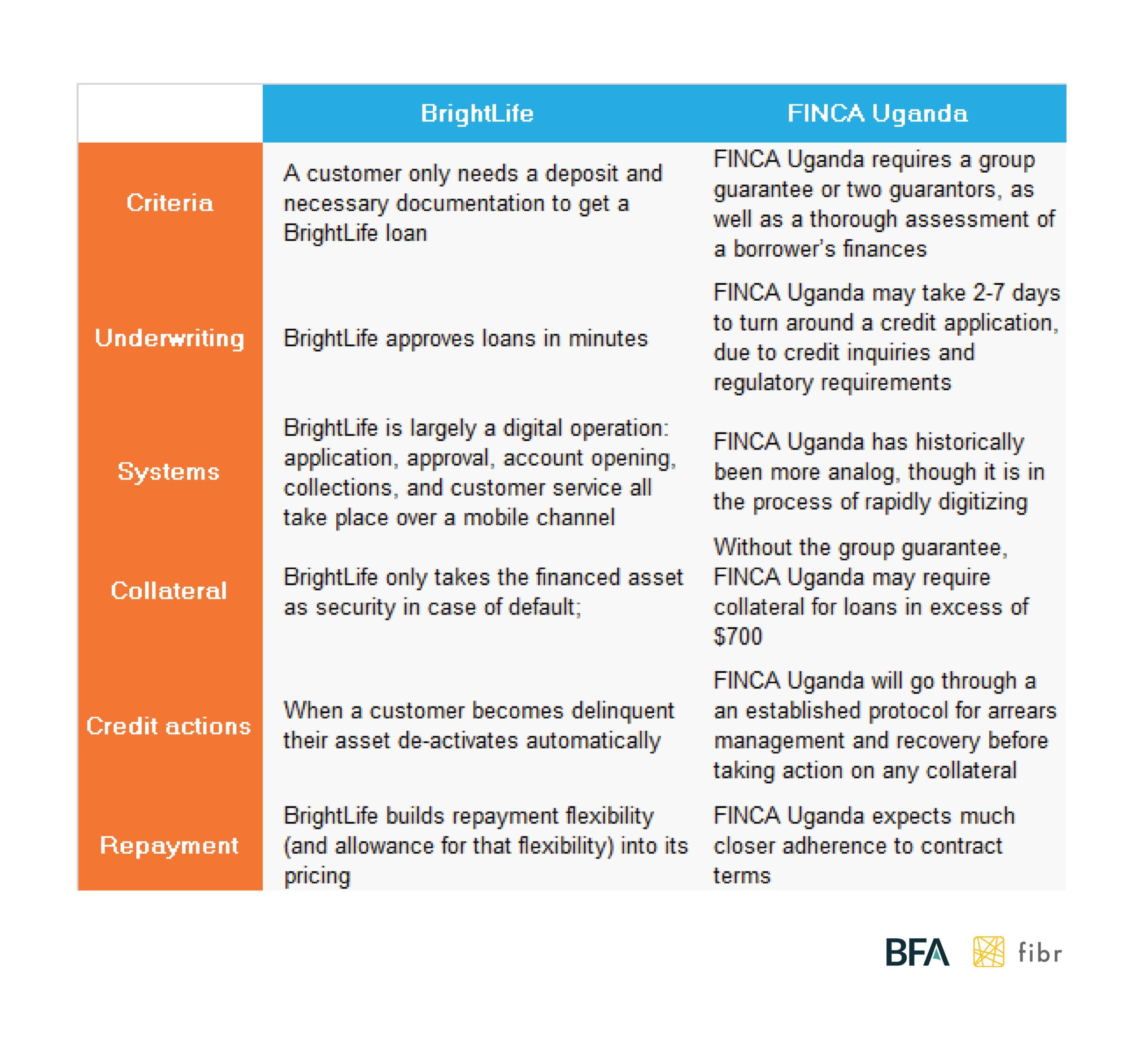

There are key differences in how BrightLife — a PAYGo operator — and FINCA Uganda — an MFI — structure and manage credit.

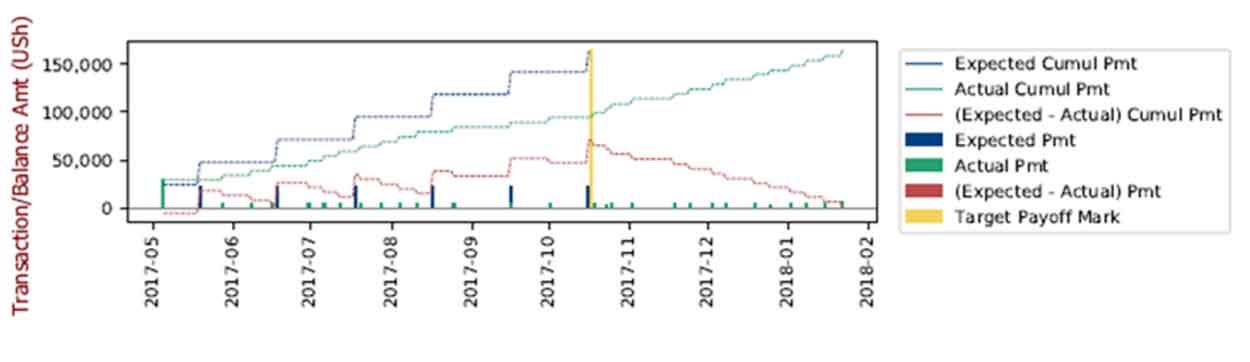

Consider a concrete example: the graph below depicts the repayment of a 6-month BrightLife loan for a solar lantern. The blue line is expected payment; the green line is reality. The customer eventually paid the loan in full, but 2.5 months late. PAYGo providers generally want this type of customer: someone who demonstrates commitment and eventually repays. They reverse-engineer their pricing to cover higher losses and lower repayment while ensuring the product remains affordable (that is how you end up with 24–36 month loans). For a microfinance institution like FINCA Uganda, this approach isn’t feasible. They need clients to pay in full and on time for the model to work. Our new product, Prosper, seeks to bridge the gap between these two lending approaches.

Challenge #2: User Goals & Preferences

“I would prefer to pay in cash; I don’t want to be pressured” — customer

Most BrightLife customers we spoke with had similar financial goals: to pay for their children’s education (a huge challenge in Uganda), to grow their businesses, and to build resiliency for inevitable health or climate shocks. However, while some clients want credit to finance these expenses (save down), others prefer to save up the amount. We wanted to use PAYGo loans as a starting point for supporting their larger goals, while staying cognizant of these preferences:

- Customers want liquidity. The average respondent had 3.2 sources of income and 3.5 formal or semi-formal accounts, in addition to borrowing from friends and family. They want to be able to access their money at will.

- Some customers want to save up for big items like a solar home system, while others prefer to purchase on credit and pay later (i.e., save down).

- Most customers do not want to pledge significant collateral beyond the financed asset, while a minority were fundamentally opposed to debt from a formal financial institution (a category that did not include BrightLife but did include FINCA Uganda).

Product Iterations

“I hate loans because they can make you bankrupt” — customer

To address these challenges, we created a product to transition PAYGo solar clients to become MFI clients. Our product needed to appeal to both borrowers and savers, and help clients achieve larger financial goals. Designing the product was difficult because PAYGo loans are small, and larger financial goals are, well, large. An ideal product also needed to be replicable over multiple cycles to create progressively larger waves of capital.

We struggled to find a product that would appeal to savers and borrowers, and experimented with two product designs before landing on the final design for Prosper. Our first prototype offered access to formal credit from FINCA Uganda to those BrightLife clients who paid for their solar product on-time. This prototype was well understood, but appealed only to “borrowers”, thereby excluding “savers”.

The second prototype increased daily PAYGo charges, and allocated a portion of every payment to savings, which could then be used as collateral for a loan from FINCA Uganda. This prototype was confusing for most people, though they found the savings attractive once it was explained. However, customers quite naturally wanted to deposit and withdraw at will, which presented operational challenges since BrightLife and FINCA Uganda needed clients to maintain sufficient balance to simultaneously finance the PAYGo product and serve as collateral for a loan.

In the end, we went a different route: a conditional rebate that customers could only access once they paid for the PAYGo product in full.

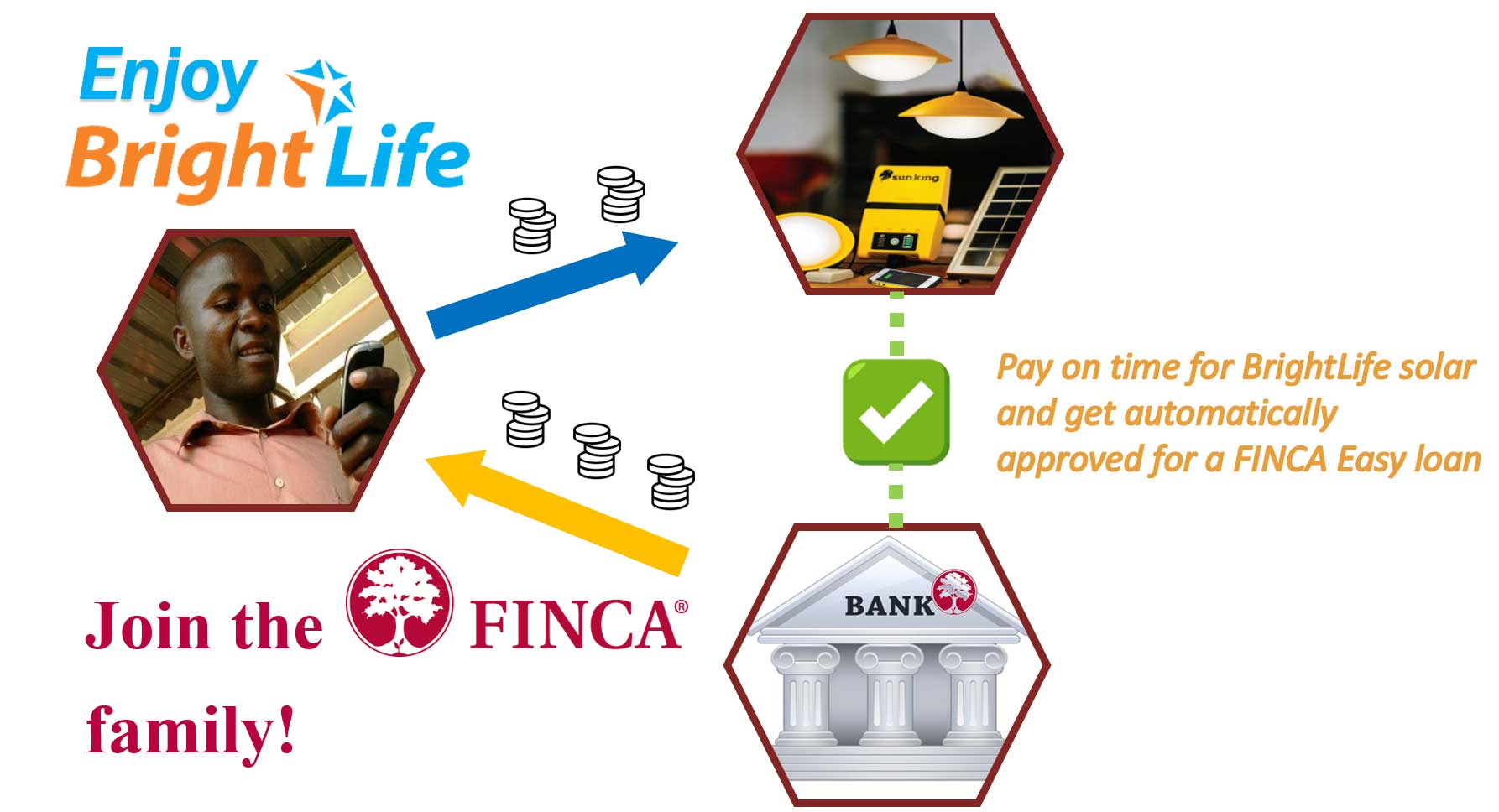

Prosper

The final product — Prosper — has three basic parts: Light Up, Grow, and Prosper.

1. Light Up

The first part is the core PAYGo asset loan, but with slightly higher prices in order to accommodate the conditional rebate. While the deposit is unchanged, the tenor is increased to 12 months and the daily rate is slightly higher. Even with these changes, BrightLife’s daily cost is still among the lowest in the market, and the loan one of the shortest PAYGo products on the market.

2. Grow

When customers finish paying for the Light Up asset, they receive a lump sum rebate equivalent to 20 percent of their total payments. The only requirement for receiving this sum is to have finished paying for the asset. The rebate can be used in three ways:

- Deposit into a FINCA Uganda account (as savings and possibly loan collateral)

- Serve as a down payment for a new BrightLife asset (e.g., a solar-powered TV, fuel-efficient cookstove)

- Transfer to a customer’s mobile money account (to be used at their discretion)

3. Prosper

Customers who repay their Light Up loan on time AND deposit their rebate in a FINCA Uganda account can access a loan from FINCA Uganda using the deposit as collateral. The loan will be up to two times the value of their Light Up product, and clients can use it to invest in their business or meet short-term liquidity needs, such as school fees. The exact amount of the loan depends on variables such as repayment speed, days missed, consistency, and others.

Addressing the Challenges

The Prosper product responds to customers’ preferences by:

- Providing additional liquidity and flexibility in the repayment of the Light Up loan, options for use of the rebate, and greater overall access to financial services.

- Allowing for both saving-up and saving-downs; clients can opt to grow their initial deposit from the rebate, or leverage their good solar repayment to access additional credit for assets or businesses.

- Not requiring customers to pledge physical assets in order to access credit.

This solution also has advantages for the individual institutions. BrightLife gets distinct marketing advantages through the rebate and credit, which also incentivize full and on-time repayment of the asset loan. FINCA Uganda gains a viable channel to acquire qualified new clients, who they otherwise would not be able to reach.

Remaining Challenges

However, the institutional differences around credit (Challenge #1) remain somewhat unresolved. The follow-up Prosper loans are traditional microfinance loans, very different from BrightLife’s PAYGo approach. In the short-term, both organizations are cognizant of the need to provide constant support during the transition process as customers may find the switch difficult.

In the medium-term, the FINCA Impact Finance network announced plans to embrace fintech innovations like mobile savings and credit products, and remote account opening. These innovations are more like BrightLife’s lending culture and may ease the journey from PAYGo to microfinance.

Once the Prosper product has been piloted, there are several further possibilities for collaboration. FINCA Uganda can explore using lockout technology as collateral for loans, which could enable lower costs or higher loans limits. They could also continue using the loan-rebate structure to help clients build wealth, similar to the minimum savings requirements that some MFIs employ. And BrightLife can experiment with financing larger appliances and system upgrades on a wider scale. Once we have more data we look forward to revisiting this subject in future blog posts and papers.