Emerging Dynamics for the Future of Agent Networks

Even though mobile and financial technology are advancing rapidly, banks and telecoms still manage agent networks just as they did ten years ago. They are still using the same techniques borrowed from fast-moving consumer goods (FMCG) and experiencing the same problems of high costs, low activity, unbalanced liquidity, and uneven customer experience.

To address this, we have released a new paper, Digital Solutions for Analog Agents: New Technologies to Manage Agent Networks, which analyzes the largest issues facing agent network managers and considers potential solutions that could be built from scratch or borrowed from adjacent industries.

Ultimately, we found that the pathway to developing solutions was not clear. Would it be better to create an end-to-end management solution or craft customized solutions for specific operational issues? Should these solutions target big corporate banks and telecoms, dynamic new start-ups, or a meso-level of master agents and retail chains in-between?

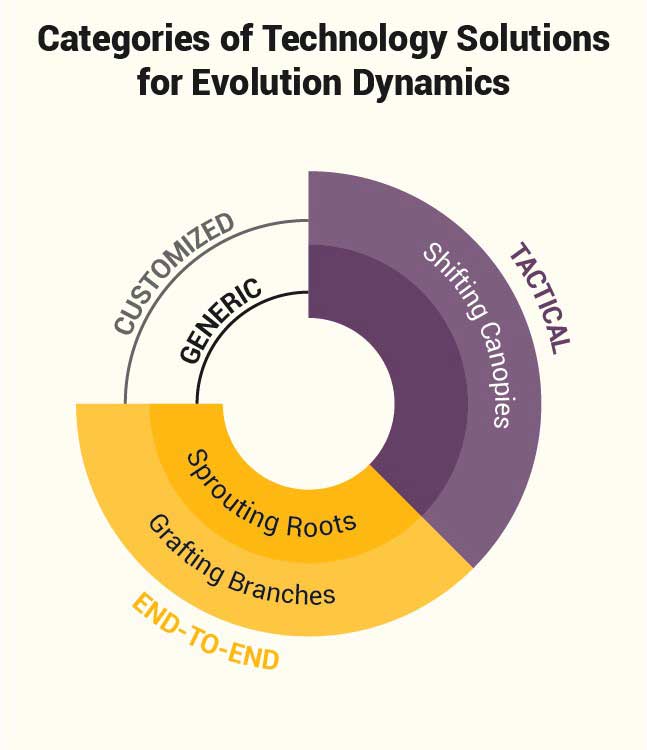

The short answer to these questions is: it depends. Any of these approaches could help based on how digital finance ecosystems evolve. We use the metaphor of a tree to describe how dynamics on three different levels of agents networks have the potential to drive them forth and the implications for technology strategies to improve them.

1) Shifting Canopies: Telecoms no longer own agent networks

In Sub-Saharan Africa, McKinsey found that telecom shareholder returns dropped 60% between 2011 and 2016, and the GSMA predicts annual growth rates in the region will decline until 2021. This is largely because growth was fueled by a period of new customer acquisition that is ending, and average revenues per user (ARPUs) are low in comparison to other regions.

These pressures are creating a period of cost shedding and consolidation, with players selling infrastructure like towers and consolidating in markets with more than two providers. In this environment, telecoms may sell, license, or spin-off their agent networks, creating a shift in who owns the network and who is allowed to offer products over it.

New owners or operators of these large networks looking to improve their operations would need to build customized patchworks of technologies from scratch. This is because agent networks come in all shapes and sizes, and operators would want to focus tactically on priority operational issues, as opposed to complete solutions.

Questions: While this is possible, the industry has yet to see this happen. Therefore, it is still unclear who would buy such an asset. Technology companies do not want to manage businesses with such large operations components, even though they might benefit from being able to offer products using them. Sales and distribution companies may not be interested in assets with such antiquated systems unless they were able to sign-up big customers that justify the types of investments needed.

2) Grafting Branches: Master agent expansion to serve multiple providers

In urbanized developing countries and in regions like Latin America, where large retail chains were used to recruit agent networks, these networks could grow into powerful independent distributors. This is also possible in countries with large master agents, who could become independent.

Technology solutions for master agents would also have to be custom-built for the existing management of the master agent. However, growth will be a much higher priority in this scenario than the first, as the master agent will want to aggressively expand into more regions of the country. Therefore, master agents would probably want an end-to-end management system that helps them do everything from agent selection to quality management.

Questions: While there are already examples of this dynamic like PesaPoint in Kenya, Selcom in Tanzania, and Eko in India, they are still rare. Master agents need successful providers to enable their growth, and then they need to negotiate with the rivals of their original partner to be able to distribute their products. Few master agents can do this without ruffling too many feathers, and even fewer have the sophistication to manage these relationships at scale.

3) Sprouting Roots: New tech-based players grow their own networks

In ecosystems where agent networks are not meeting demand, new technology-based players could grow their own agent networks. Countries like Nigeria, where telecoms have been prohibited from building networks, or Zambia, where corporations have been slow to invest, are open opportunities for start-ups like Pagatech and Zoona to sprout.

Further, interoperable ecosystems should make it easier for independent operators to service multiple providers and transact with their clients without needing to sign contracts with each provider. We have also seen social enterprises building their own networks, especially in rural areas without mobile money agents where they do both distribution and payments.

Finally, start-ups will definitely seek end-to-end solutions but might be willing to buy something off-the-shelf to save money. The management system would have to be flexible enough to work in differing regulatory environments and adapt as the network grows, but it may only offer generic settings at the start.

Questions: Thus far, these models have only worked in sheltered environments where large corporations have been prohibited from playing or have chosen not to. If policy shifts in Nigeria so that telecoms could build agent networks or if telecoms in Zambia make aggressive investments, these smaller models might be quickly crushed, calling into question their longer-term viability.

Each of these different dynamics will require distinct technology solutions, whether end-to-end or customized for priority operations. While the shifting canopies dynamic means that it is possible that existing networks could open up to distribute financial products from an array of different companies, the second two scenarios both involve growing new players to a large enough scale to compete.

Either way, technology will be critical to the evolution of the ecosystem to improve operational efficiencies and customer experience, to drastically cut costs, and to catalyze growth for new kinds of companies. This makes it a crucial topic for the future of agent networks everywhere.

For those interested in learning more about the potential of technology to revolutionize agent networks, please find our paper here: Digital Solutions for Analog Agents: New Technologies to Manage Agent Networks.