How Does the Inclusive Fintech Landscape Compare to Mainstream Fintech?

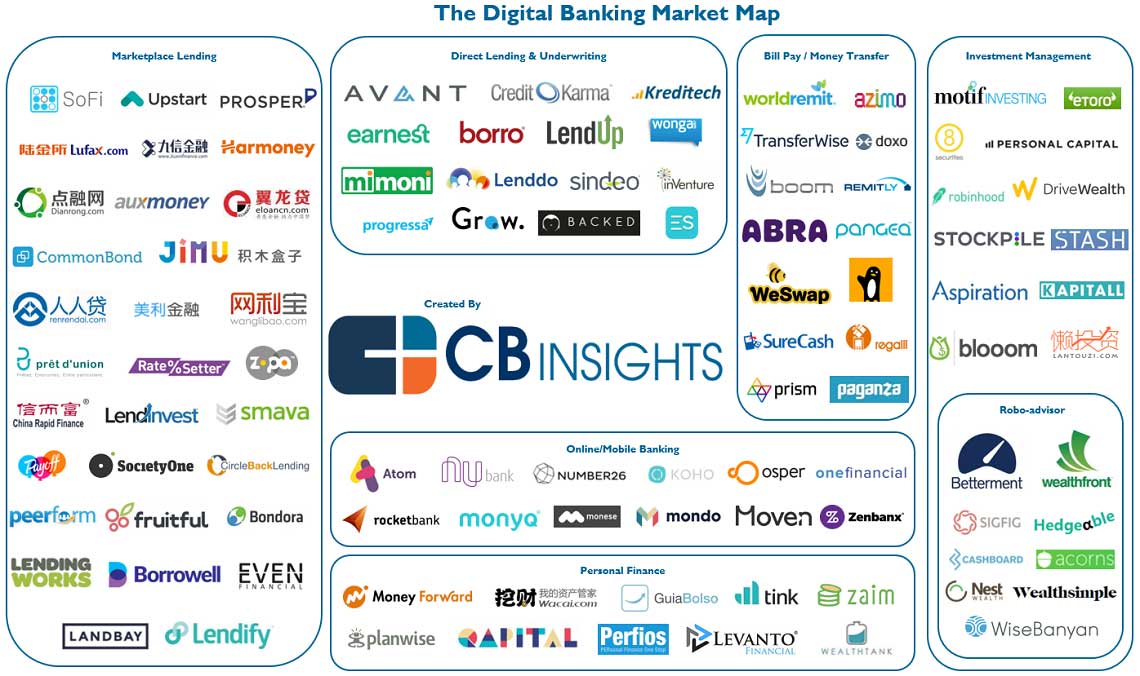

In the last few years the fintech sector in developed markets has gone through a phenomenal boom. Fintech is the intersection of financial services and technology approaches, typically provided by a startup company. Arguably PayPal was the first fintech company, founded in 1998. There weren’t that many more successful cases until well after the dotcom crash. But recently, there’s been a lot of activity populating this space as illustrated in the diagram below:

All combined, the startups in this wave are posing a serious challenge to the established financial incumbents, who are scrambling to join the revolution and co-opt the most dangerous players.

This wave of innovation is being fostered by a handful of enabling factors:

- Consumers now have smartphones that can allow them to access apps and websites when and where they need them

- In addition, the financial crisis left consumers ready to change to better and cheaper providers of financial services

- The resources to build a financial service are plentiful and affordable, specifically:

- Pretty much every consumer in the rich world has a digital bank account

- There are lots of data available about each and everyone of those consumers

- Cloud computing is cheap and there are many available algorithms to crunch data

- Many of the above resources can be tapped over APIs

- The investor community has poured billions of funding into these novel approaches. Over US$13.8 billion was deployed to a wide variety of fintech companies globally, more than double the value of VC investment in fintech in 2014 (CB Insights, 2016).

- There are many hungry entrepreneurs ready to enter the fray

Inclusive Fintech in Emerging Markets

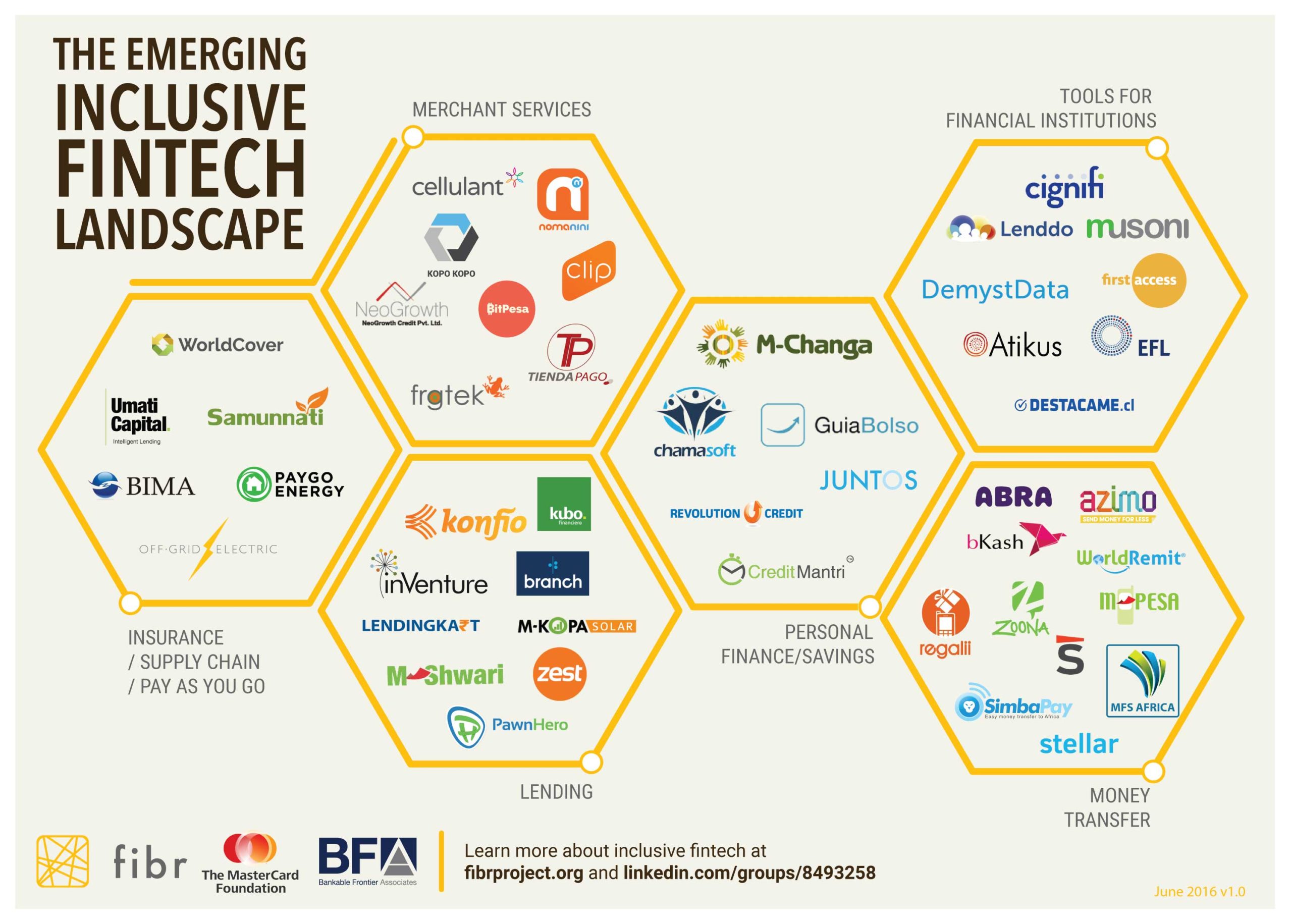

However, the fintech situation isn’t as booming when you look at emerging markets. In particular, the number of startups leveraging fintech approaches to include the underbanked isn’t as large as in the developed world. As a parallel to PayPal, you could argue that M-Pesa was the first successful example of inclusive fintech. Unfortunately, we don’t have many more available examples — this is what we think the inclusive fintech landscape looks like:

The probable reason is that the following enabling factors in inclusive fintech aren’t fully in place yet:

1: Smartphones aren’t as prevalent, even if they should be by 2020.

2: The demand from consumers although very high, remains mostly untapped by the microfinance movement.

3: Unlike the rich world, not every poor consumer has a digital store of value. Also, those offered by mobile money providers are rarely available through APIs. Furthermore, there isn’t that much data about low-income consumers. On the brighter side, anyone anywhere can leverage cloud computing for the same plummeting price.

4: There are not that many investors deploying capital behind these fintech initiatives. Fortunately, there are much bigger amounts in the traditional microfinance investors that hopefully can be mobilized to fuel a disruption wave.

There are many talented entrepreneurs pursuing fintech opportunities like the winners of the Zambezi Prize or those in the portfolios of investors like Accion Venture Labs and Omidyar Network. Like every other digital revolution, inclusive fintech could significantly broaden the customer base by lowering costs and boosting value propositions. So the stakes are high, and you could argue this is the way to offer everyone a decent set of financial services.

What are BFA and FIBR doing about it?

One of BFA’s newest project is FIBR. The mission of FIBR is to fund and test new business models that foster indirect financial inclusion instead of going by the traditional direct relationship (a financial institution trying to market to a low-income customer). The FIBR, indirect model leverages trusted relationships of small businesses, such as a shopkeeper, with their customers, in their local communities as an access point to financial services. Furthermore, by capturing the increasing amount of user data now available on smartphones, inclusive fintech players can explore financial services that are designed around how the customer engages in business in their daily lives.

FIBR supports and partners up with local entrepreneurs. During 6 month engagements, the teams then quickly design and test inclusive fintech products and services with an eye to scaling rapidly. In the coming weeks, FIBR will announce the new set of partners in Ghana covering inclusive fintech innovations in agriculture, education and merchant services. The insights gathered from FIBR partner engagements will be shared with the industry at large so that other funders or entrepreneurs have a new source of ideas and inspiration in the blossoming inclusive fintech landscape.

Like you, we would love to see the inclusive fintech landscape full of impressive successes. We’ll be doing our bit to help some of the most relevant prospects. So we will be periodically updating the landscape to keep track of this rapidly shifting movement over the life of FIBR!